We use cookies and similar technologies to recognise your repeat visits and preferences, as well as to measure the effectiveness of campaigns.

By clicking Allow, you agree to the use of cookies in accordance with our Privacy Policy.

Learn more.

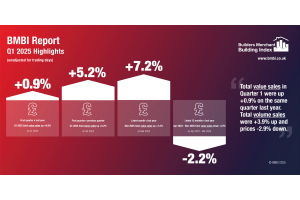

BMBI Report - Q3 2023 Highlights

December 06, 2023

Builders’ Merchant Q3 volume down -10.5% on Q2 2022. Value sales down -3.3%.

Compared to the same period in 2022, Q3 2023 total volume sales to builders and trades fell -10.5% from Britain’s Builders’ Merchants. Value sales were down -3.3%, as prices rose +8.0%. There was no difference in trading days. The three largest categories all sold less: Heavy Building Materials (-1.5%), Landscaping (-7.0%) and Timber & Joinery Products (-13.1%).

Q3 results weren’t helped by September total value sales, which were -6.1% down on September 2022, with no difference in trading days. Volume sales fell -13.0% and prices rose +7.8%. Heavy Building Materials (-5.8%), Landscaping (-6.7%), and Timber & Joinery Products (-13.9%) all sold less.

Quarter-on-quarter, total value sales dipped -1.4% in Q3 2023 compared with April to June 2023. Volume sales dropped -2.1% and prices edged up +0.8%. With four more trading days in the most recent period, like-for-like sales were -7.5% lower in July to September compared to Q2.

Nine of the twelve categories had higher value sales quarter-on-quarter, with Kitchens & Bathrooms (+7.5%) increasing the most. Landscaping (-13.3%) was weakest.

Compared to August, total merchant September value sales were down -3.4%. Volume (-2.7%) and price (-0.7%) were also down. With one less trading day in September, like-for-like sales were +1.2% higher. Only three categories sold more: Workwear & Safetywear (+2.7%), Plumbing, Heating & Electrical (+2.3%) and Kitchens & Bathrooms (+0.8%). Seasonal category Landscaping (-9.2%) contracted the most.

Mike Rigby, CEO of MRA Research who produce this report, said: “Quarter 3 was a wash out for the building industry. From the unrelenting rain which put a halt to outdoor work in August and September, sending homeowners abroad in search of the sun, to the drop in housebuilding output which fell to its lowest levels since Covid, not much was happening.

“GfK’s Consumer Confidence Index also fell sharply from -21 to -30 in October defying expectations of continued improvement to -20 as the high cost of living and economic uncertainties weighed on sentiment. But with inflation dropping more than forecast, from 6.7% in September to 4.6% in October, a year after the dismal days of Prime Minister Liz Truss, will the Chancellor’s Autumn Statement lift the national mood and get Britian building, and growing, again? There’s a lot of resilience in the private housing repair, maintain and improve sector. If you doubt it, try finding quality trades who are not busy and booked into 2024, for your home improvement project.”

Developed and run by MRA Research, the BMBI – a brand of the Builders Merchant Federation - is a monthly index of builders’ merchant sales, and the most reliable, up-to-date measure of Repair, Maintenance, and Improvement (RMI) activity in the UK. The index is based on actual sales from GfK’s Builders’ Merchant Point of Sale Tracking Data, which captures value sales out to builders from generalist builders’ merchants, accounting for over 80% of total sales from builders’ merchants throughout Great Britain. An in-depth review, which includes commentary by sector experts, is provided each quarter.

The Q3 2023 BMBI report is available to download at www.bmbi.co.uk.

Account Summary

Short Code:

Credit Limit:

Current Balance:

Recent Posts