We use cookies and similar technologies to recognise your repeat visits and preferences, as well as to measure the effectiveness of campaigns.

By clicking Allow, you agree to the use of cookies in accordance with our Privacy Policy.

Learn more.

BMBI Report - January 2023

April 03, 2023

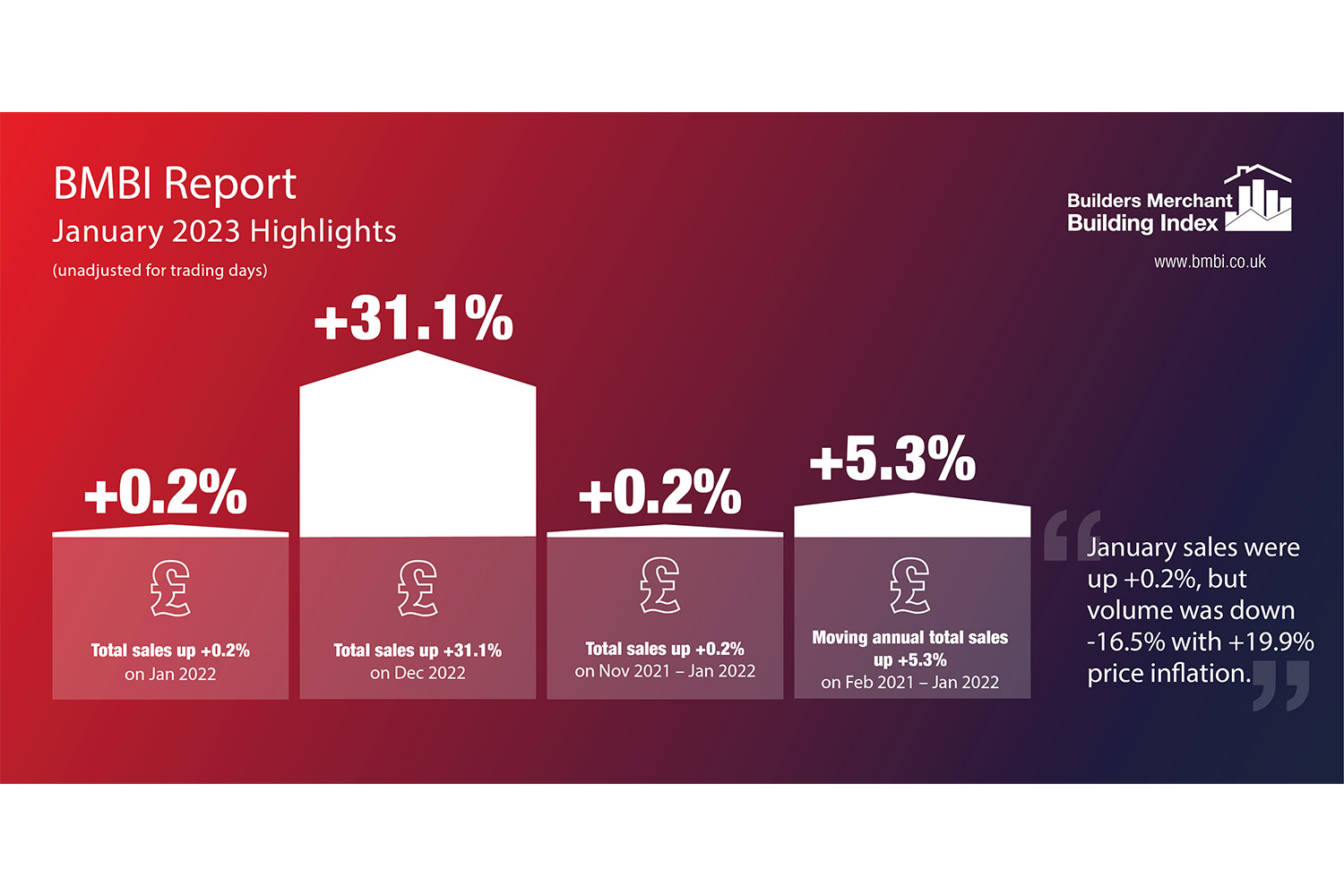

January merchant sales marginally up but volumes still down year-on-year

The latest Builders Merchant Building Index (BMBI) report reveals that builders’ merchants’ value sales were up +0.2% in January 2023 compared to the same month in 2022. This nominal growth came largely from inflation as volume sales were down -16.5% while prices rose +19.9%. With an extra trading day this January, like-for-like sales were -4.6% lower.

Nine of the twelve categories sold more in January compared to the previous year. Renewables & Water Saving (+46.0%) continued to perform strongly, while Decorating (+20.5%), Plumbing, Heating & Electrical (+17.5%), Workwear & Safetywear (+14.4%) and Kitchens & Bathrooms (+12.4%) also did better than overall sales. Timber & Joinery Products (-14.6%), Landscaping (-11.8%) and Services (-0.5%) sold less.

Month-on-month, total merchant sales were +31.1% higher in January 2023 than seasonal low month, December 2022. Volume sales also grew sharply (+28.6%) with price slightly up too (+1.9%). With five more trading days in January, like-for-like sales were flat (-0.1%). Renewables & Water Saving (+49.6%) grew the most, followed by Ironmongery (+38.0%). Services (+10.2%) was the weakest category.

Total merchant sales in the twelve months from February 2022 to January 2023 were +5.3% up on the same period a year before. Price inflation was a double digit +16.5% while volumes were down -9.6%. With two less trading days in the most recent period, like-for-like sales were +6.2% higher. Ten of the twelve categories sold more with Renewables & Water Saving (+32.5%) and Kitchens & Bathrooms (+17.7%) the standout categories.

Emile van der Ryst, Key Account Manager – Trade & DIY, GfK comments: “Market turmoil in the past year has now reached the stage where some of the monthly figures need further context. This month, January-on-January sees a +0.2% value increase, with a -16.5% volume decrease and a +19.9% price increase. Logic dictates that value should therefore be around +3-4% if volume and price are balanced against each other. This month is however affected by Heavy Building Materials, Timber & Joinery and Landscaping distorting the total market view.

“These three categories combined make up around 75% of total market value, and therefore heavily influence topline trends. But they are each quite different in the mix. Heavy Building Materials has one of the lowest average prices of the categories but has seen a larger than market average price growth. At the same time, Timber & Joinery has one of the highest average prices, but has seen lower than market average volume declines, with prices declining against rampant total market inflation. Finally, Landscaping is a key volume driver in the market, but has seen a larger than market average seasonal volume decline. These factors in combination occasionally create hard-to-understand distortions, unexpected anomalies in topline trends which need to be seen in context.

“We expect these trends to continue through 2023 and into the first half of 2024 as inflation, demand and supply gradually return to a more normal stability. Where possible GfK will try to add further context to explain these trends.”

Developed and run by MRA Research, the BMBI – a brand of the Builders Merchants Federation - is a monthly index of builders’ merchant sales, and the most reliable, up-to-date measure of Repair, Maintenance, and Improvement (RMI) activity in the UK. The index is based on actual sales from GfK’s Builders’ Merchant Point of Sale Tracking Data, which captures value sales out to builders from generalist builders’ merchants, accounting for over 80% of total sales from builders’ merchants throughout Great Britain. An in-depth review, which includes commentary by sector experts, is provided each quarter.

January’s BMBI report, published in March, is available to download here.

Account Summary

Short Code:

Credit Limit:

Current Balance:

Recent Posts